On 14-15 June, we attended Intersolar Europe 2023, Europe’s largest solar and renewable energy exhibition in Munich, Germany. This year, a record number of 2,469 exhibitors and 106,000 visitors from 166 countries attended the event. The high participation rate (vs. 1,356 exhibitors and 65,000 visitors from 149 countries in 2022) makes the perfect rebuttal to concerns that Europe’s enthusiasm for the green transition has faded after energy prices and electricity tariffs have been falling since mid-2022. And, we came back more positive to the solid growth trends in the solar industry and believe that the energy transition continues to present many attractive investment opportunities.

To start with, we see the strong momentum in the growth of solar installations continuing, if not accelerating. According to SolarPower Europe, EU’s solar industry association, global new PV installation reached 239GW in 2022, a 45% year-on-year (yoy) growth from 2021. This means that the total global solar capacity has surpassed 1,000 GW. SolarPower Europe expects another boom year for 2023, with an estimated new addition of 341GW to the grid, or 43% growth from 2022. Even with the high growth rates, we still see exciting potential for further PV penetration, given solar PV only meets 4.5% of global electricity demand in 2022, while over 70% is still provided by non-renewable sources.

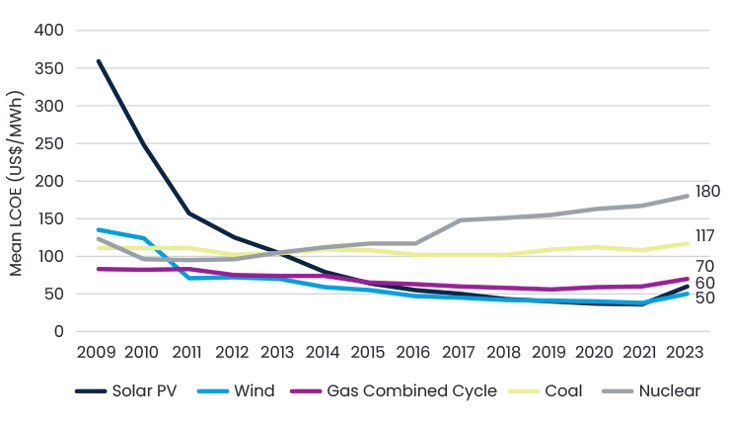

Solar’s remarkable success can be attributed to numerous factors, but a key driver is its significant cost reduction over the past decade, propelling it to become the global leader in terms of cost competitiveness. However, the past two years have witnessed significant supply chain disturbances, lingering COVID-19 effects, and inflationary pressure worldwide, sparked by the war in Ukraine. All this has caused the first increase in solar’s levelised cost of electricity (LCOE) in over a decade. That, however, does not pose a challenge to cost competitiveness; solar PV remains significantly cheaper than new fossil fuels and nuclear, and product prices already began to decline in recent months and are largely expected to return to pre-crisis levels soon.

Levelised Cost of Energy Comparison

In addition, we expect China to remain a dominant player in the global solar value chain, unlikely to be shaken by global localisation efforts. In 2022, China maintained its leadership position in new solar PV installation of 94.7GW, representing 40% of the added total global capacity. This is more than four times the second-largest market, the United States, and larger than the other top nine markets combined. With an expected annual growth rate of 49% in 2023, China’s global market share will increase further to 41%. In terms of PV manufacturing, China plays an even bigger role. From upstream polysilicon to downstream PV panels, China has maintained over 90% global market share throughout the years and will see higher market share on the back of a slew of new projects to be completed in the coming years.

Many investors question if we will see decoupling of global markets from the Chinese solar value chain. In 2022, the United States’ solar market recorded 21.9GW of new installation, a 6% decrease yoy, driven by anticircumvention investigations relating to anti-dumping tariffs and the Uyghur Forced Labor Protection Act (UFLPA). However, one significant source of uncertainty has reduced after President Biden introduced a tariff exemption for two years on solar modules manufactured in Southeast Asia by the Chinese players. At the same time, the European Union (EU) is driving solar growth through its Green Deal and REPowerEU initiatives, but experts from Fraunhofer ISE, the largest solar research institute in Europe, argues that the effort of building a local supply chain in Europe will be costly (at least 2-3x more than in China) and will take at least 3-5 years to reach only 10-20% of EU solar demand. Therefore, in the short-to-medium-term, green transition without China seems impossible.

Another key issue watched closely by industry participants and investors is the price dynamics of polysilicon in the past two years. Polysilicon is the upstream raw material used to produce solar wafers and represents roughly 40% of the production cost of a solar panel. The price of polysilicon had been on an upward trajectory for the past two years, peaking at around 330rmb/kg (>40usd/kg) in November 2022, compared to just around 80rmb/kg (c. 12usd/kg) in early 2021. The sharp price increase was caused by an imbalance between supply and demand when capacity expansion could not catch up with demand increase. The upward trend of polysilicon price has sharply reversed since the end of 2022 and is back at below 70rmb/kg (<10usd/kg) level, thanks to the ramping up of all the new capacities after extended periods of construction that started in the past two years.

By closely following the supply and demand dynamics across upstream and downstream players, we position our portfolio towards companies that will benefit the most from market development in the coming 6-12 months. One change that we made over the last year was to exit from our polysilicon exposure, which enjoyed great profitability when product prices were high, and instead we shifted to the downstream panel and inverter makers. We expect the downstream players to enjoy volume growth boosted by lower supply chain prices as well as sharp margin recovery thanks to the profit redistribution from material cost reduction. Based on the current market price of polysilicon, we estimate Jinko Solar, a leading solar panel manufacturer in China, will earn a net profit twice as much as what the current street consensus expects in 2023. This also implies that the shares of the company are only trading at 2.4x 23pe, which presents us with a great investment case for a global leader in the fast-growing solar industry.

Documents & links

Related articles