In our 2024 Outlook, we suggested that 2024 would be an ‘alpha’ year, with a slightly more benign global environment allowing investors to focus on company fundamentals. Although the year was far from plain sailing, our prediction seems to have played out, at least for us. All our funds delivered strong alpha for our unitholders – an achievement that we are very proud of. We believe that the key factor behind this success is our core investment philosophy, which emphasises in-depth, on-the-ground research to understand company quality, combined with a strong awareness of the broader market drivers, including behavioural aspects.

2024 in retrospect

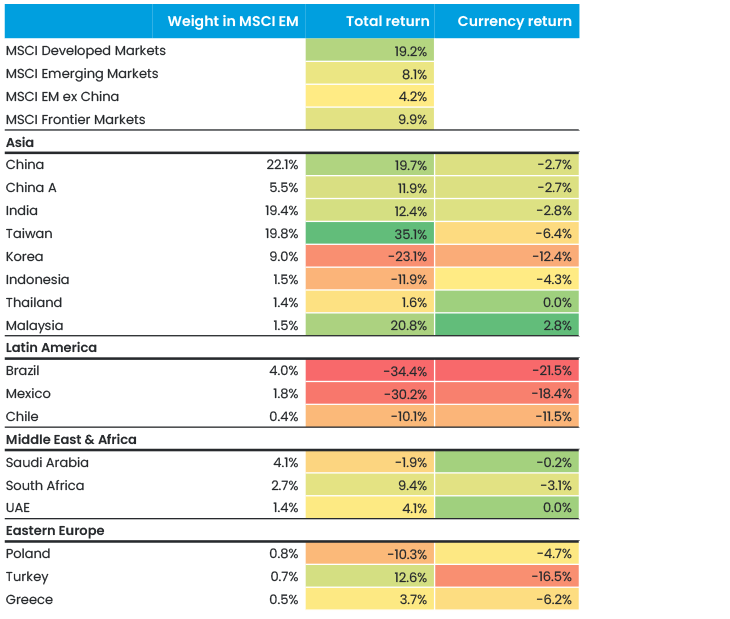

2024 saw a highly varied range of returns in both emerging and frontier markets (Figure 2). This illustrates our long-held view that these are a group of inherently diverse markets at different points in their cycles, with specific market drivers. This naturally requires a slightly differentiated investment approach for each market, something we are increasingly focused on. For example, what works in India – is unlikely to work in Brazil or China.

Taiwan stands out

Taiwan was the clear standout performer in 2024, returning 35% as investors piled into the AI theme. The largest name in the benchmark, and in our fund, TSMC, reached a market capitalisation of USD 1 trillion in Q4 2024, returning 74% for our Global Emerging Markets fund during the year. This performance was largely driven by earnings revisions, as the highly sophisticated AI chips it makes for Nvidia offer significantly higher margins, which is why the company consistently raised its margin guidance throughout the year. Q3 revenues were up 36% year on year, but profits were up 54% as a result of this margin increase.

Figure 2. Emerging market returns in 2024

China outperformed, surprising many

The Chinese market ended the year up 19.7%, outperforming developed markets, which may come as a surprise to most people. We have commented extensively on China throughout the year, for example in this detailed article. In general, we are seeing some improvement in the country. The government clearly understands how bad the situation is and has acted forcefully to address the key issues. At the very least, their actions show that they are not prepared to let things get much worse, which puts a floor under the stock market.

Going forward, we believe the government will do what is necessary, but in incremental, small steps that will take time. While this may disappoint some of the more vocal Western investors, we expect China will end 2025 in a much better position than it started the year, which should be supportive for markets, especially given the country's highly attractive valuations.

Alpha drivers - India on top

Looking at our flagship global funds, we were pleased that alpha was spread widely across countries. In our Global Emerging Markets Sustainable fund, our largest alpha generator in 2024 was India, where our holdings returned 41%, compared with 11% for the benchmark's Indian holdings. We note that, given our broadly country-neutral approach, this alpha was generated purely from stock selection rather than a ‘bet’ on India.

India is in many ways a classic emerging market, benefiting from strong structural growth but also from a thriving local investor base. Indeed, the country is so large and dynamic that there are over 1,000 companies with a market capitalisation of over USD 5 billion. Even with the strong market performance, we are still finding attractive new companies with strong growth that are trading at reasonable valuations.

In our Global Frontier Markets fund, Vietnam and Nigeria were the standout contributors, collectively adding over 12% of alpha. Vietnam experienced a challenging year, with the market down 5.4%. However, our holdings returned a remarkable 29%, driven by IT company FPT; this is the largest position in our fund, at nearly 10% weight, and it achieved a 75% return for the year. Meanwhile, Nigeria was removed from the index, although our well-timed trades benefited from the subsequent performance as the country eased capital controls and introduced a number of other market-friendly reforms.

A milestone anniversary for our Global Frontier fund

December was a milestone month for our Global Frontier Markets fund as it celebrated its tenth anniversary. Over the past decade, the fund has generated an impressive alpha of approximately 70% compared with the MSCI Emerging Markets and around 90% versus the MSCI Frontier Markets, all while offering reduced volatility due to the low correlations between markets. We therefore believe the fund is worth a look for those investors who want to reduce overall portfolio volatility without sacrificing returns.

35 years since the fall of the Berlin Wall

In November 2024, we celebrated the 35th anniversary of the fall of the Berlin Wall, a momentous event that marked the beginning of a new era of growth and transformation across Eastern Europe. This opportunity inspired the creation of East Capital in 1997, as we sought to actively contribute to and participate in the region’s development.

27 years later, we remain deeply committed to Eastern Europe and believe the investment opportunity remains as exciting as ever. In a world of stretched valuations, Eastern Europe stands out, looking relatively cheap despite a solid macro backdrop, with growth three times above the EU average. The region trades at record low valuations of around 7x P/E despite earnings growth of around 20% and dividend yields of around 6%, with banks yielding 10%. A sustainable peace deal in Ukraine could be a major trigger for the region, which has traded at a significant discount to emerging markets since the war broke out.

A difficult year for sustainability

In many respects, 2024 was a challenging year for sustainability, marked by increasingly negative rhetoric from the US and heightened scrutiny of renewable project returns due to rising interest rates and a complex permitting process.

Although we have made significant investments in the renewable energy supply chain over the past five years, our current portfolios have minimal direct exposure to pure-play renewable energy. Instead, we generated substantial alpha in other, more investable sustainability themes, such as recycling, water treatment, education, and healthcare.

We remain committed to collaborative engagements, including active participation in the Net Zero Engagement Initiative, where we are involved in three engagements. We also co-lead two major engagements with BYD and CATL in collaboration with the Asian Corporate Governance Association (ACGA).

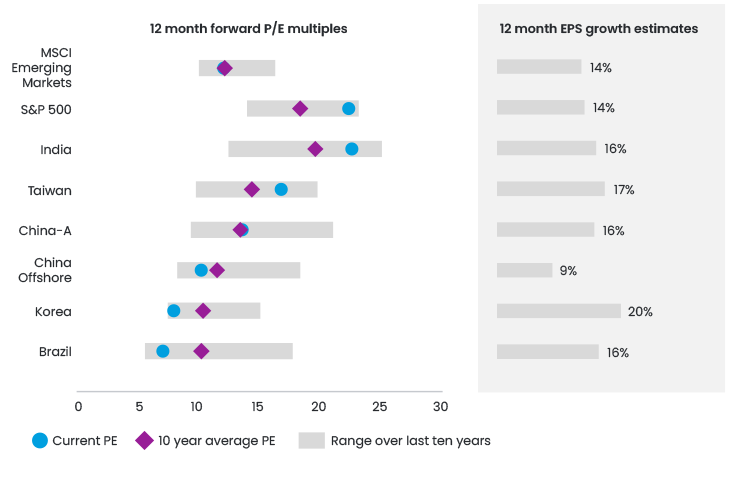

Figure 3. 2025 Outlook – a lot of the news is in the price

What lies ahead?

We encourage you to read our 2025 Outlook for a detailed view of our expectations for the year ahead. In short, we believe that many of the widely discussed issues have already been priced in and are reflected in the current valuations. For example, it is well known that China is at risk of tariffs and its economy isn’t doing very well. As a result, markets like China and Brazil look very cheap on a historical basis, while markets like India and Taiwan are more expensive. Overall, however, this means that emerging markets are trading at historical levels (Figure 3), while the US looks incredibly expensive. This makes emerging markets a compelling consideration, particularly for diversifying away from the US, as other regions, such as Europe, face potential struggles.

Emerging market earnings growth is projected to be 14% in 2025, and we see this as a reasonable estimate of returns for the year, although there will clearly be many developments throughout the year that will push this up or down.

Related articles