Emerging and Frontier Markets Outlook 2025 – Another alpha year?

2024 was a solid year for emerging and frontier markets, both returning 12% in USD terms as of 10 December. We expect the positive momentum to continue into 2025, based on decent earnings growth and with much of the bad news largely priced in and reflected in positioning. JP Morgan estimated earlier this year that global funds had around 5.3% allocated to emerging market equities. A return to the 20-year average allocation of 8.4% would result in inflows of USD 910bn, or 58% of current emerging market assets under management. As such, we think emerging and frontier markets are worth a look given the rather demanding valuations and concentration in the US.

The specific path of returns will likely be determined by the key 'known unknowns', namely the exact nature of Trump's tariffs and their impact on US inflation and global monetary policies, as well as whether the Chinese government can revive the country's flagging economy. However, there will inevitably be many more 'unknown unknowns' that will emerge as the year progresses. As a result, we believe that 2025 (like most years) will be a year for dynamic stock pickers who are prepared to adapt quickly to changing conditions and take advantage of any mispricing that occurs.

2024 – a mixed bag

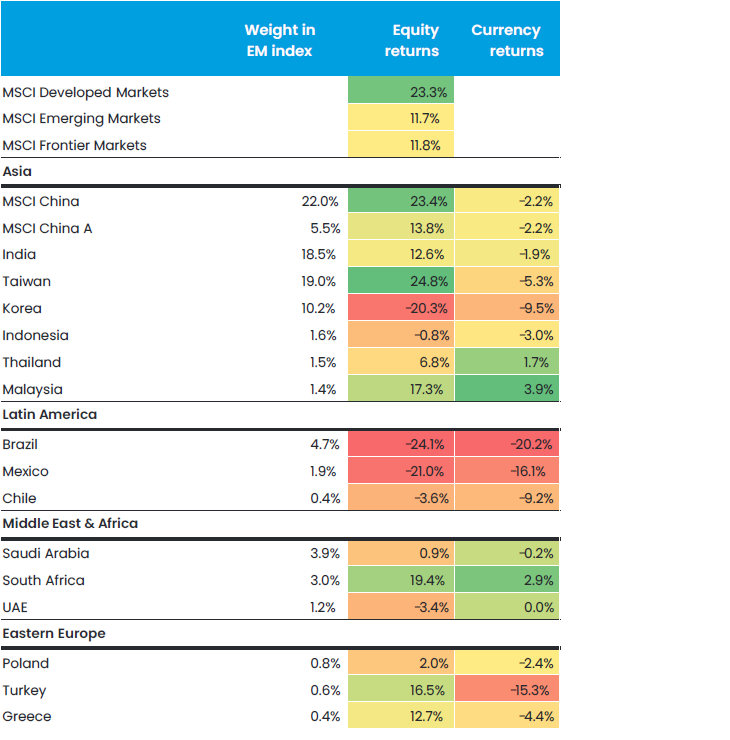

The returns in 2024 illustrate one of our key theses, which is that emerging markets are a very heterogeneous group of countries, all at different points in their cycles and with diverse market drivers. The standout market in 2024 has been Taiwan, which is driven by the AI theme as it produces all the advanced AI chips for Nvidia, which benefits the largest holding in our global emerging markets strategy, TSMC, but also its suppliers. It is likely a surprise to most that the China offshore market outperformed developed markets, returning 23.4%.

It is also important to note that the underperformance relative to the US has not been due to lower earnings growth. In fact, East Capital Global Emerging Markets Sustainable ("GEMS") portfolio saw earnings growth of around 25% in 2024 and is expecting 18% next year, or a compounded earnings growth of 48% over two years. In comparison, S&P 500 earnings growth over the two year period is expected to be 26%.

Figure 1. Total USD returns YTD up to 09.12.24

In line with our previous outlook that 2024 would be an "alpha year", many of our holdings have significantly outperformed their respective markets. For example, in our current GEMS portfolio, there are 19 out of 57 stocks that have returned more than 50% (in USD, as are all return figures), 8 stocks that have returned more than 100% and 1 stock that has returned more than 200%. This final stock was Korean company Hyundai Electric that produces transformers for the global market.

These outperformers were generally driven by a handful of key themes that we have focused on during the year. We highlight the themes that we believe will continue to offer good opportunities in 2025 in Figure 2.

Figure 2. Key themes for 2025

High shareholder returns

- Particularly in China (and increasingly Korea), companies are increasingly focussed on returning capital to shareholders in the form of dividends and also buybacks

- We are pushing management to cancel bought back stock, which can have a significant impact on EPS growth; for example Qfin is likely to cancel around 9% of the share count every year for the next three years, which will significantly improve EPS; together with the generous dividend, we expect a yield of 12%

- However, we can find high yields across the world, with Halyk Bank in Kazakhstan offering 20%+ yield for 2025, Mexican education company Laureate Education offering 10%+ or 13% for Kuwait education company Humansoft

Global electrification

- Electricity consumption from data centres, AI and the crypto sector likely to double by 2026 vs 2023, with data centre demand expected to double between 2022 and 2026, where they will demand 1,000 TWh in 2026, equivalent to the electricity consumption of Japan

- Transformers are one of the biggest bottlenecks currently, with our Korean transformer exporter Hyundai Electric up 283% YTD in USD

- Our largest holding in Latin America is the “Siemens of Emerging Markets” WEG, that is a beneficiary of the weak local currency and also the transformers boom in the US; we also like smaller more niche names like Cenergy in Greece

Financial inclusion

- 50% of Mexicans don’t have a bank account which presents exciting opportunities for companies like Nubank and also microfinance company Gentera

- This is a trend we see across our markets, with dominant fintech Kaspi in Kazakhstan, Kenya’s Safaricom with their digital wallet or even Indian wealth manager Nuvama Wealth

Recycling, water treatment and climate

- Particularly in India, there are various regulatory tailwinds that mean we have high visibility for exceptional earnings growth

- This will be highly beneficial for companies such as lead recycler Gravita, or plastic recycler Ganesha Ecosphere, which recycles over 7 billion plastic bottles a year and so has excellent access to feedstock

- Water treatment is another area offering strong structural growth as government spending kicks in; we like VA Tech Wabag here

- Finally, we like names such as Empower in UAE, which is the world’s largest district cooling company, essentially pumping cool water around building, which is up to 50% more energy efficient than air conditioning

Education and health

- These sectors offer classic structural growth stories in emerging markets due to underpenetration and growing middle classes

- We like Indian healthcare companies growing at 50%+, whereas in China we prefer education, which is one area parents’ won’t save money on

- More broadly, education tends to be highly cash generative, with high visibility recurring revenues, and here we like companies like Laureate Education in Mexico/Peru and Best Study in China

On the negative side, clearly Latin America stands out. This was largely due to self-inflicted wounds by the countries’ politicians that hurt the currency and the equity markets. However, coming back to our alpha year argument, our two largest names in Brazil (WEG and Nubank) returned 57% and 41% respectfully, thanks to strong structural growth regardless of the macro backdrop – this is huge outperformance compared to the - 24% of Brazil.

Looking forward – a positive backdrop

Globally, macroeconomic conditions remain relatively benign, with solid economic growth (i.e. neither hard nor soft landing) and falling interest rates in most countries. This has historically been a good backdrop for equity markets.

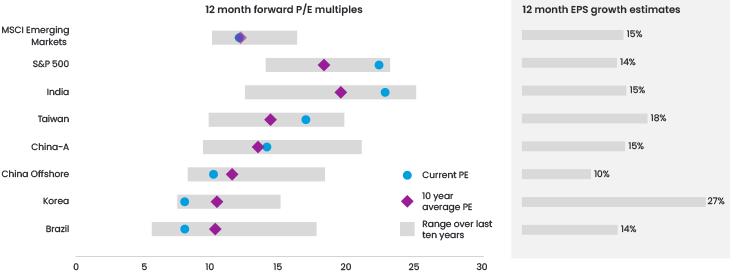

Under Trump 2.0, the US is the most obvious winner, thanks to expected tax cuts, deregulation and a likely strengthening dollar. However, this is priced in, with the US trading at near 10-year highs (Figure 3) and with a record weighting in global benchmarks, e.g. 65% of the MSCI All-World Index versus 50% 10 years ago. As such, it is not surprising to see views such as this recent FT article which refers to the current US market as “the mother of all bubbles”. The main argument is that while US stocks were more expensive during the dotcom bubble in 2000, the US market did not trade at nearly as large a premium to the rest of the world.

Figure 3. Next 12 months valuations and earnings growth

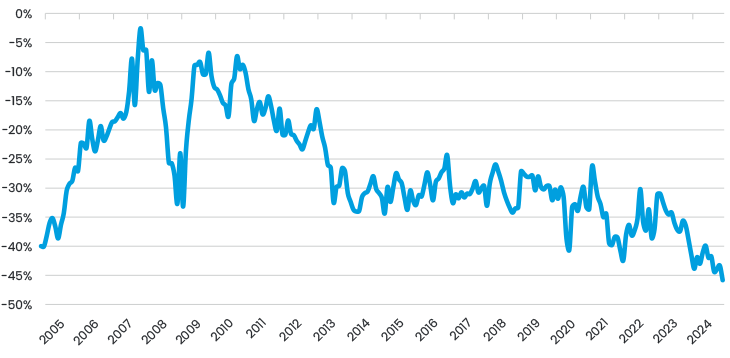

Emerging markets, on the other hand, are trading around average valuations on an aggregate basis and at a 45% discount to the S&P 500, which is a record high discount (Figure 4).

Figure 4. Emerging markets discount to S&P 500 over time

We do not expect emerging and frontier markets to significantly outperform the US, but given the record high valuations and global portfolio investors’ concentration in the US, we think it is worth looking outside Wall Street for a portion of portfolios. And the pickings outside the US are slim: Europe remains on life support, with the "sick man of Europe" Germany posting 0% (not a typo) GDP growth this year and well below 1% in 2025. On the other hand, overall emerging markets’ economic growth looks reasonable at 4.5%, with the second largest market, India, expected to grow 6.5% next year thanks to structural growth that is completely uncorrelated to the US.

This article will therefore focus on what we see as the main drivers for some of the key regions and markets in which we invest.

China – can the dragon roar again?

For all the doom and gloom, Chinese equity markets have had a very good year, outperforming the emerging market asset class, with MSCI China up 23% YTD in USD, in line with developed markets, while domestic A-shares index is up 14%.

Members of our team based in China report that the situation is improving slightly. Clearly the government understands just how bad the situation is and has acted forcefully to address the key issues. At the very least, their actions show that they are not prepared to let things get much worse, which puts a floor under the stock market. Going forward, we believe the government will do whatever it takes, but in incremental, small steps, that will take time. The view we hear from the London-based investment community, is even more positive, i.e. that the Chinese government has had a "whatever it takes" moment and will continue until they have addressed some key problems in the economy, which should happen next year, and so the market should do well because it is extremely cheap. We are slightly more cautious, due to the deep rooted structural issues consumers and businesses are facing – as we wrote in a recent article on China, if you give someone a USD 100 cheque, it won’t make them spend more if they are worried about losing their job.

The government is taking a methodical approach, focusing on the two main systemic risks: the housing market and local government debt. This was demonstrated by the unveiling in November 2024 of a USD 1.4 tn debt programme, which swapped the expensive off-balance sheet hidden debt of local governments for longer-term and cheaper public loans. Many of these local governments have simply not paid their bills for various services because they are so strapped for cash. Anecdotally, we've heard stories of nurses or teachers in certain provinces not receiving their salaries - this has clearly had a ripple effect throughout the regional economies. The other big question mark is about the property market, and we haven't seen any bazookas being used yet, with the government preferring a drip-feed approach to policy, although the USD 550 bn of support for 'white-listed' property developers will help with liquidity issues.

Tariffs will continue to dominate the headlines. China's exports to the US accounted for only 2.8% of GDP in 20231, including re-exports, with less than 15% of Chinese exports going to the US, and with more exports going to other countries such as Southeast Asia, indicating the rise of the “Global South” as a major buyer of Chinese goods. Moreover, less than 2% of MSCI China's earnings come from US exports, and we know these companies so can easily avoid them. Of course, a 10% tariff is different from a 60% or 200% tariff, so we remain in wait-and-see mode. With the appointment by Trump of mainstream economists to the key financial posts, such as Scott Bessent as Treasury Secretary and Kevin Hassett as Chair of the National Economic Council, we can expect a more rational approach than a full-blown trade war which could have been in the cards if he had re-appointed former US Trade Representative Robert Lighthizer who orchestrated the first set of tariffs in 2018.

Figure 5. China exports by destination

When we look at equities, we always try to understand what the market's expectations are, what is already priced into the stock. For China, we think a lot is priced in - do you know anyone who doesn't expect more tariffs on China or doesn't know how bad the economy is? That is why hedge fund long positioning is at record lows (e.g. first percentile over five years). This is also reflected in overall valuations, but particularly in the valuations of the high-quality defensive names we like to own in the country. For example, Alibaba is trading at free cash flow yields of 10-12% for 2025 and 2026, and buying back USD 4-6bn of stock a quarter, versus a market cap of USD 214bn.

This illustrates a key factor that further reduces the downside - instead of issuing equity at a relentless pace, Chinese companies are now buying back stocks and paying dividends. Looking just at A-shares (where the data is better), buybacks in 2024 year-to-date are double what they have been over the past five years (Figure 6), and we think this number will continue to grow in 2025 based on what we are hearing from companies. As mentioned above, shareholder returns are a key investment theme for us going into 2025, and also in our engagement with companies.

Figure 6. Total buybacks in China A-shares market (RMB 100 mn)

India – growth on track despite speedbumps?

India has been one of the emerging market success stories over the past few years, outperforming the S&P over most time periods. As such it is now the second largest market in the MSCI emerging markets index, and so a major driver of returns. This performance has been driven by a booming economy, which was in turn driven by government capex, and a retail investor boom, with USD 60 bn of domestic inflows into the market year-to-date.

The mood in Mumbai is now surprisingly subdued – the country is entering a cyclical slowdown, with a relatively weak (by Indian standards) GDP print of 5.4% in Q3 2024. Government capex, which has been one of the key engines of growth over the past few years, growing at a 30% CAGR over the past three years, has recently shrunk by 35% YoY. This was largely due to the general elections in mid-2024, and will clearly improve, which is why we have some confidence that this is a cyclical slowdown rather than something more significant.

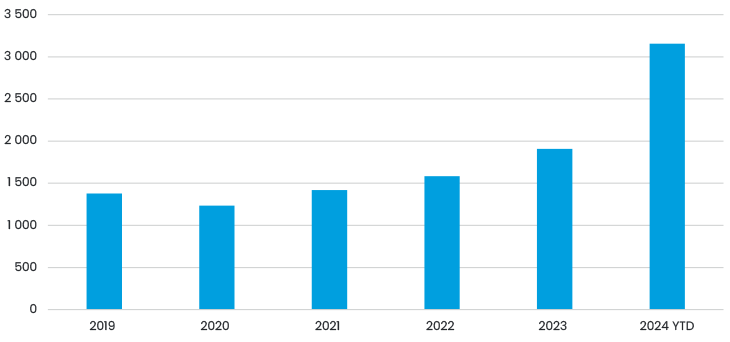

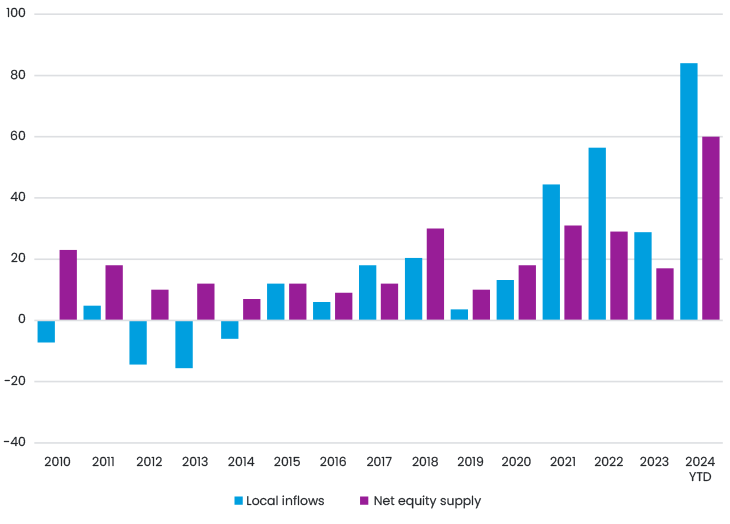

However, the trajectory of this increase in capex is unclear, which becomes a concern given that Indian stocks are not cheap, with consumer names such as Hindustan Unilever trading at 50x P/E for this year whilst offering earnings growth of just 5%. Moreover, the high valuations have not gone unnoticed by companies, and there is a constant flood of equity placements, which are sucking up market liquidity and flows, as we show in Figure 7.

Figure 7. Local inflows and net equity supply in India (USDbn)

Nevertheless, the structural long-term growth story for India remains intact, driven by favourable demographics and stable governance. Furthermore, historically low levels of corporate and bank debt position the country well for the next phase of growth. India is also relatively more insulated from global shocks, including tariffs from the incoming Trump administration, as external balances remain resilient.

As such, we believe the outlook for India remains positive on a 12-month basis, although it certainly remains a market that requires a very active approach. For example, we have recently taken profits on many of our mid-cap names, that have rallied 100% or more, and rotated into some of the large caps. Having said this, through our newly opened research hub in Mumbai we still are finding interesting mid-cap opportunities in areas like healthcare or recycling.

Elsewhere in emerging markets

Taiwan is in many ways a pure-play AI exposure, given the dominance of TSMC (over 50% of the country in the MSCI Emerging Markets benchmark), which is the only company in the world sophisticated enough to produce Nvidia's advanced chips. If you believe in the continuation of the AI boom, which seems to be accelerating rather than slowing down given the investment plans of the "Magnificent 7", we think Taiwan will become a larger allocation for global funds focused on broadening the AI theme. This should continue to drive performance as valuations are not expensive relative to the US. We also like to look beyond the chip companies, and see interesting opportunities in simpler industries such as bicycle companies.

The political and geopolitical situation in South Korea has deteriorated rapidly in 2024, with the imposition of martial law and escalating tensions with North Korea. This is one reason why the country's returns have been so poor year-to-date. Going forward, we expect the noise on both fronts to continue, although hopefully to subside somewhat. On the positive side, we see that the "Value-Up" programme, which we have written about here, is starting to gain traction. This was most evident when the largest company, Samsung Electronics, announced a USD 7.2 billion buyback programme (around 3% of market capitalisation). The company is sitting on USD 75 billion of cash and we think this is the least of what can happen. With P/B valuations at 0.9x, compared with 3.4x in Taiwan and 1.5x in Japan, there is clear upside if companies continue to make material improvements in governance.

Latin America has also had a torrid year, so much so that it is hard to imagine things getting much worse. However, after the appalling lack of fiscal discipline in Brazil and the legal reforms in Mexico that have significantly undermined the rule of law, we believe it will take some time for these markets to regain investor confidence. We remain very conservatively positioned, focusing on companies whose earnings streams are relatively uncorrelated to the economy and which have strong balance sheets and are therefore not affected by the persistently high interest rates. One example of this is Weg, “the Siemens of emerging markets”, which generates 50% of its sales outside Brazil.

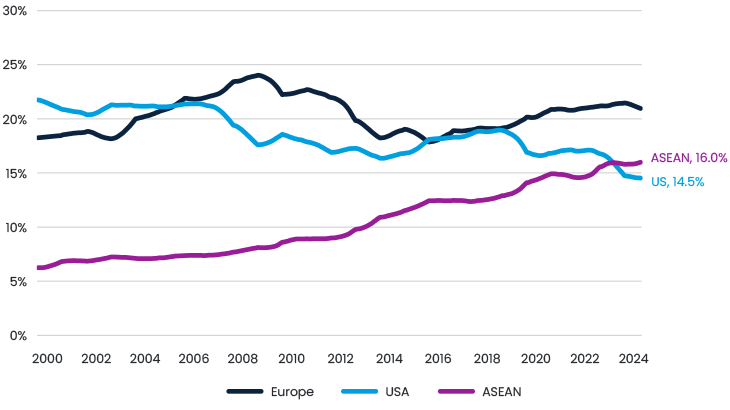

Eastern Europe – a value investor’s dream

In a world where valuations are stretched almost everywhere you look, Eastern Europe stands out as looking fairly cheap despite solid macro, with growth 3x above the EU average. The region trades at record low valuations of around 7x P/E despite earnings growth of around 20% and dividend yields of around 6%, with banks yielding 10%.

The counterpoint to this view is that a slowing Europe (particularly if exacerbated by Trump tariffs on cars) will be a drag on growth and sentiment, so it will be important to follow the news flow around tariffs.

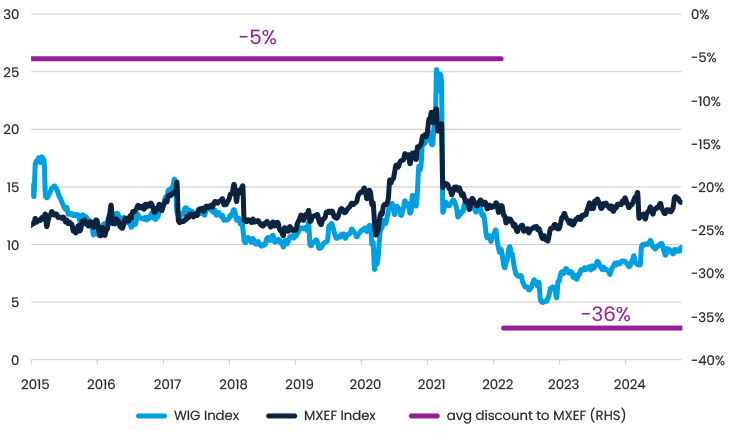

The main trigger for a re-rating would be a sustainable peace agreement in Ukraine. This is clearly evidenced in Figure 8, which shows Poland’s valuation relative to emerging markets - historically it has traded at an average discount of 5%, but since the invasion of Ukraine in 2022 this discount has fallen to 36%, even though the macro has been solid.

Figure 8. 12 month forward PE in Poland vs MSCI Emerging Markets index (MXEF)

Frontier and small emerging markets remain uncorrelated and reasonably priced

Frontier markets economies should continue their upward trajectory in 2025, supported by improving macroeconomic conditions, easing inflation and attractive equity valuations. While global uncertainties around Fed policy and trade tensions persist, frontier markets remain well positioned to capitalise on local growth drivers. In addition, low correlations to developed and emerging markets continue to act as a buffer against global volatility.

In Asia, Vietnam is forecast to grow by 6.1% in 2025, driven by its integration into global supply chains and strategic trade agreements. Renewed trade tariffs could pose both upside and downside risks to Vietnam as a manufacturing hub, but the expected FTSE upgrade of its USD 200 billion stock market to emerging market status, most likely in Q1 2025, should increase liquidity and investor interest. The Philippines, also forecast to grow by 6.1%, is benefiting from resilient remittances and domestic consumption. Inflation is expected to remain manageable at 3%, providing a stable economic backdrop and making its stock market, trading at 10x 2025e P/E, particularly attractive.

The Middle East remains a bright spot, underpinned by the transformation agendas in Saudi Arabia and the UAE. Saudi Arabia's Vision 2030 reforms are expected to drive GDP growth of 4.6%, led by expansion in non-oil sectors such as technology and tourism. The UAE is forecast to grow by 5.1%, driven by a population boom and continued public investment. Both markets are likely to see continued IPO activity, further diversifying their equity markets and attracting foreign capital. The region also benefits from USD-pegged currencies, which provide a natural hedge against global currency volatility.

In Africa, key reforms in Nigeria and Kenya are unlocking potential despite ongoing challenges. Nigeria has made notable progress under President Tinubu, with fiscal adjustment and FX liberalisation improving sentiment and reducing currency pressures. Kenya's economic rebalancing and focus on technology-driven growth offer a promising outlook. Egypt is recovering from a sharp currency correction in early 2024 and increased GCC investment inflows, although structural hurdles remain.

Overall, frontier markets offer a compelling mix of strong structural growth and diversification benefits, appealing to investors seeking uncorrelated opportunities. Key valuation metrics remain near all-time lows, with 2025e P/E of 7x offering an attractive entry point. With structural growth rates outpacing developed markets and increasingly stable macroeconomic frameworks, frontier markets offer a unique combination of resilience and upside potential.

Sustainability

As is often the case, we continue to see the world confusing sustainability with the green transition. We wrote about the green transition under Trump 2.0 in this recent article. Although we have invested heavily in renewable energy companies over the past five years, we currently have very little pure-play exposure in our portfolios as we believe that the combination of continued high interest rates, permitting issues and oversupply in China for value chain names such as panel manufacturers means that there is much more visibility and higher quality growth to be found elsewhere. That said, we continue to like the sustainability lens as a way of highlighting interesting structural growth themes such as recycling, water treatment, education and healthcare. We don't expect this to change much in 2025, as the issues we have highlighted are not going away.

Conclusion

In short, it seems that most of the known unknowns are largely priced in, which is why China and Brazil look quite cheap, emerging markets as a whole are trading in line with average valuations and the US looks quite expensive. This can also be seen in positioning, which is very light.

Our best guess is that expected returns will be in line with earnings growth, which currently stands at 15% in USD terms for emerging markets, although this figure is revised down every year, not least because of the steady depreciation of currencies against the USD.

We think China will come out of 2025 in much better shape than it leaves 2024, although it won't necessarily be the thriving economy it was a few years ago. This would still be a positive outcome given the extremely low positioning and attractive valuations. Outside of China, markets such as India and Taiwan look expensive, but will be driven by their own growth drivers: structural growth and AI capex, respectively. And in these markets and elsewhere, we believe we can find attractive and reasonably priced growth opportunities. For example, our Emerging Markets fund trades at 11.8x P/E for 2025, in line with the index, despite forecasted earnings growth of 18% versus 15% for the benchmark; earnings growth for 2024 and 2025 combined is 48%. Our Global Frontier Markets strategy trades at even lower 2025e P/E at 7.0x, with solid mid-teens average annual earnings growth through 2024-25 period and uncorrelated return profile given locally driven economies.

1Overall gross exports accounted for 19% of GDP in 2023, with private consumption representing only 39%, well below most other countries such as US (68%) and India (60%)

Related articles