What is the impact of DeepSeek on Emerging Markets?

AI-related stocks have experienced a rollercoaster start to the year, from the excitement surrounding the announcement of the $500 billion "Stargate" investment in AI infrastructure in the U.S. to the emergence of more efficient models, such as those pioneered by China’s DeepSeek, that could reduce demand for computing power.

With growing interest in the implications of the latter for emerging market equities, we decided to share our insights more broadly.

How good is DeepSeek?

The first question is whether the DeepSeek models are as good as the US models, and whether the low costs quoted are accurate. We think there's some nuance here, i.e. the costs quoted were likely pure training costs (not R&D) and probably don't include the 10,000 H100 chips the parent company had stockpiled. As for performance, we understand that while there are certain tasks where DeepSeek outperforms GPT 4.0, the opposite is also true in other areas. Also, the former is only text-based and can’t handle images and video, which require much more processing power.

However, the general conclusion is certainly true - the company has clearly managed to get more out of its chips through software innovation and clever engineering, thereby reducing the cost of LLM development. For what it is worth, our n=1 experience with DeepSeek R2 is positive, broadly comparable to ChatGpt 4.0 and other models we have used. We particularly like the way it shares how it is thinking about the question before providing an answer (Figure 1).

Figure 1. DeepSeek R2 Output

Market impact

The timing of the news was somewhat auspicious, coming one week after the Stargate announcement and in a week when the two most directly affected equity markets, in which we invest -Taiwan and Korea - are closed for the entire week and China is closed for most of the week.

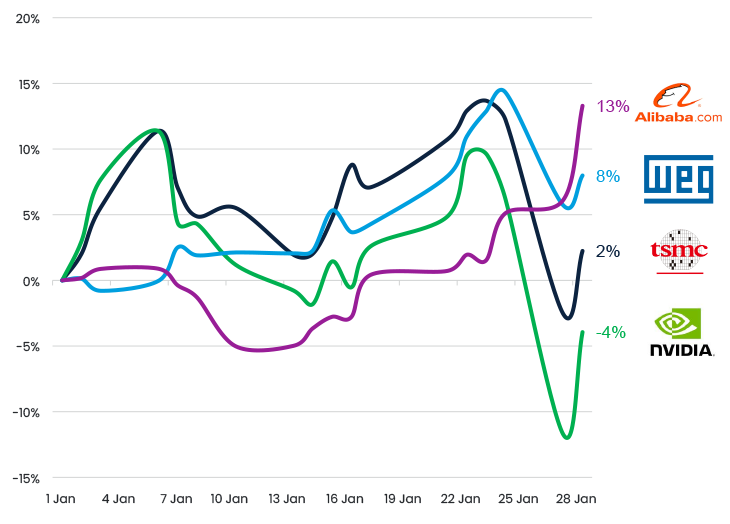

Taiwan accounts for 20% of the MSCI Emerging Markets Index, with the world’s largest chipmaker TSMC accounting for the majority at 11%. The company also trades in the US (as shown in Figure 2), and its stock has fallen 8% since Friday (24 January). Korea represents 10% of the index but is more diversified, with its largest stock, Samsung Electronics, not currently part of the Nvidia value chain.

Markets often overestimate the short-term impact of any news while underestimating the long-term impact, and may indeed be the case here. This is significant because stocks like Nvidia are clearly pricing in more than just one year of strong growth. However, it will take a while for the true impact to become clear, although it’s difficult to see chip stocks having another blockbuster year like 2024. The upcoming hyperscaler earnings calls will be important in providing guidance on capex plans for 2025 and beyond. The bullish argument was summed up well by Microsoft CEO Satya Nadella “Jevons paradox strikes again! As AI gets more efficient and accessible, we will see its use skyrocket, turning it into a commodity we just can't get enough of”. Jevons paradox states that when technological advancements improve the efficiency of a resource, and therefore the use cost goes down, the overall demand for that resource actually goes up.

In our Global Emerging Markets Sustainable fund, we have focused on the theme of global electrification, such as WEG, the "Siemens of the emerging markets". The performance of the stock is also shown in Figure 2. We believe that this theme will be a bit less in focus than it has been in the past, and therefore we have reduced our weight in WEG from a risk management perspective, as it was our largest holding in Brazil and has outperformed the Brazilian market by 45% in 2024.

Figure 2. Total return in USD YTD

China the main beneficiary?

China (28% of the emerging market index) stands out as a clear beneficiary, as one of many investor concerns was that the lack of access to cutting-edge Nvidia chips would hamper its AI capabilities. It’s not just DeepSeek that is proving this wrong. Alibaba recently published its new LLM Qwen 2.5 Max, which follows a broadly similar development approach to DeepSeek. Early results look positive based on the company’s white paper, which drove the share price up 7% on 28 January.

As such, we believe that Chinese technology stocks could start to come back on investors’ radars. Alibaba trades at 10x 2025 P/E compared to Amazon's 38x, despite a comparable product offering of e-commerce and cloud computing, where Alibaba is the largest provider in APAC. This suggests that much of the bad news on China (such as poor macro and tariff threats) is priced in. It is also worth noting that the company is sitting on USD 50 billion of net cash - equivalent to 25% of its market value - and is buying back more than USD 1 billion worth of shares per quarter.

A more under-the-radar company is Baidu, the “Google of China”. The company is on the cutting edge of AI technology, and will begin the monetisation of AI-driven search ads in 2Q 2025. Despite an 18% return in the last 2.5 weeks, the company is attractively priced, trading at only 9x 25 PE. We expect growth will start to accelerate next year, putting the stock back on investors’ radars.

Related articles