Kinas DeepSeek – ett Sputnik-ögonblick eller ett språng som inte ska underskattas?

DeepSeek R1 is an open source AI tool developed by a team funded by Wenfeng Liang, the co-founder of the Chinese hedge fund High-Flyer. Their new release, R1, has topped the free download list in Apple’s App Store since 26 January 2025, and in China we see it being used absolutely everywhere. While the exact numbers are somewhat unclear, what is clear is that DeepSeek’s approach offers enhanced efficiency which leads to huge cost advantages. Indeed, 1 million output tokens cost just USD 2 for DeepSeek versus USD 60 for OpenAI’s O1 model. There are numerous surveys of ‘how good it is’ but the Compass Academic Leaderboard ranked it no. 1 among large language models as of 13 January (Figure 1). Personally, I think it is half a notch better than the current AI applications I use, albeit these will likely improve fast. It would also not be unrealistic to expect AI models to become more efficient and cheaper, perhaps exponentially.

Figure 1. Compass Academic LLM Leaderboard as of 13.01.25

Why does it matter?

The point is not whether DeepSeek is better or worse than other AI applications, but that the processing power required and the overall cost are dramatically lower. Advanced processors, and therefore AI, are at the heart of current geopolitical tensions, with the assumption that US companies will win the race. And, while they may still win, DeepSeek has shown that there are faster horses in the race. For China, this simply means that the IT sector will get a big boost as it will certainly have 'good enough' AI to implement in various services/platforms. DeepSeek is open source, so any company can copy the code, or parts of it. One of the analysts we met this week had even copied it to build a small language model on his own laptop.

Another important point is that it is not just DeepSeek that is developing great LLMs - in Figure 1 we highlight all the Chinese LLMs in red – these are clearly competitive with the US models. Alibaba is a good example and was recently selected by Apple to power the AI on all iPhones in China, something that could contribute up to 9% of net income by 2026 according to some analysts.

It is dangerous to underestimate China

In just a few weeks, we've witnessed not only the launch of DeepSeek but also BYD's self-driving technology, God's Eye. The latter will be offered for free in most BYD vehicles, including the Seagull, which costs less than $10,000—while Tesla charges $8,000 for its self-driving feature alone, and with significantly higher vehicle prices.

Although BYD cars are unlikely to appear on US roads, the global transition to renewable energy relies on the adoption of electric vehicles. In 2024, BYD was projected to sell 4.3 million EVs and hybrids, far exceeding Tesla’s 1.8 million EV sales. However, in terms of pure EV sales, BYD was only slightly behind Tesla last year. High-quality, free self-driving technology adds another compelling reason to choose an EV, which already accounts for 50% of all car sales in China.

Where do we go from here?

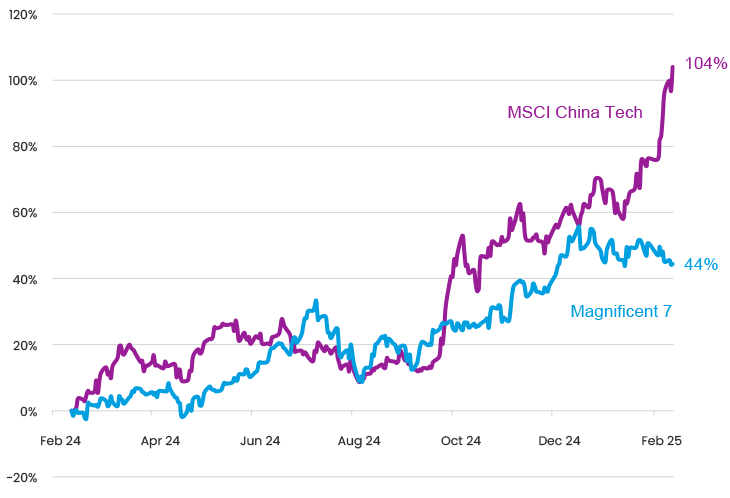

Perhaps the most important point for us is that we simply cannot ignore China. The most striking evidence of this being the performance of China's technology sector versus the MSCI All-Share Index over the past year (Figure 2).

Figure 2. Magnificent 7 versus MSCI China Tech, 12-month USD return

We don't think many investors realise just how strong this performance has been, as the sentiment on China as a whole has improved only slightly, but there is also clear evidence that it can compete on the global stage.

China remains an undervalued and unloved market - if we 'zoom out' on the chart in Figure 2, the Chinese tech sector has returned just 8% over 5 years, while the Magnificent 7 have returned 400%. This suggests that China remains cheap, but also underowned, and the last month shows how the market can perform when sentiment changes, e.g. BYD is up 30% in one month on the back of the God's Eye announcement. Alibaba is up 46% in the same period.

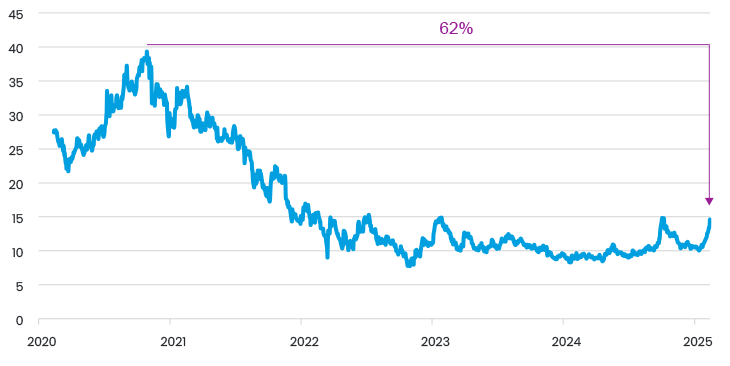

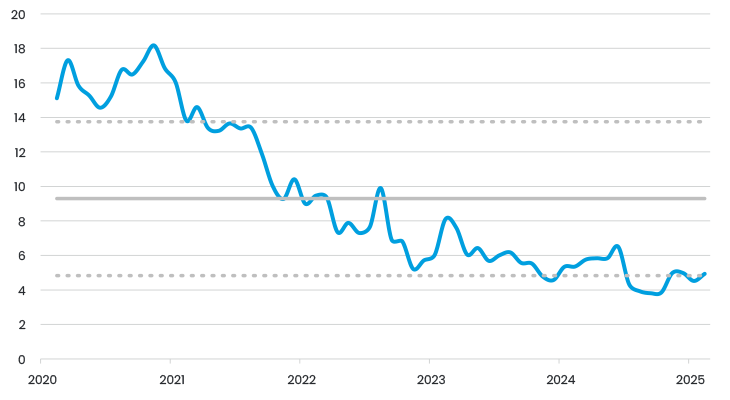

It's hard to say what's next, but this kind of price movement clearly reflects the combination of renewed interest and technological progress. Indeed, if you look at Alibaba's share price, while it has moved nicely, it is clearly still at extremely low levels in the larger context (Figure 3) and also looks relatively cheap (Figure 4). This is especially true when you consider that instead of making huge investments like the Magnificent 7, they are focusing on returning cash to shareholders in the form of dividends and buybacks - we expect the yield to be around 5.5% this year.

Figure 3. Alibaba stock price (USD)

Figure 4. Alibaba forward EV/EBITDA

We hold BYD, Alibaba and a number of other Chinese IT companies in our Global Emerging Markets Sustainable strategy.

Relaterade artiklar